What’s happening with commodity cocoa?

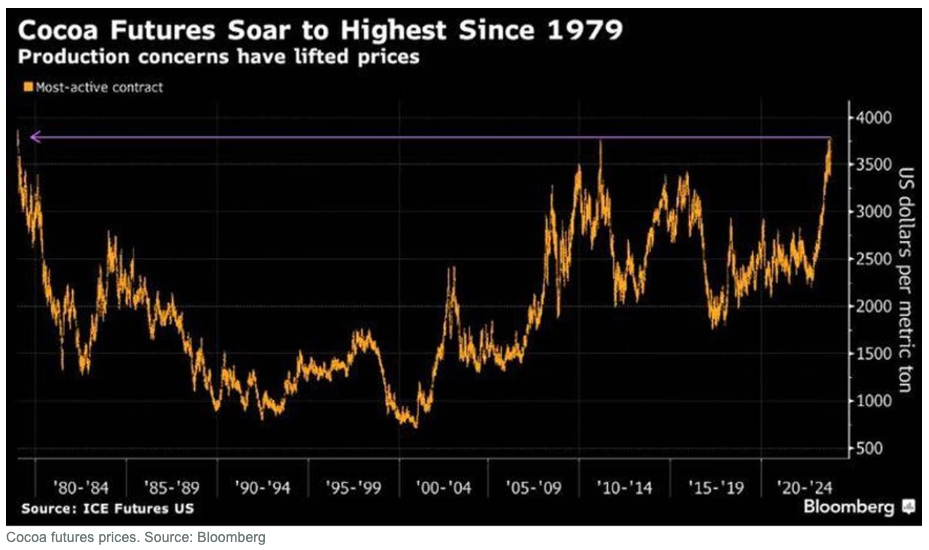

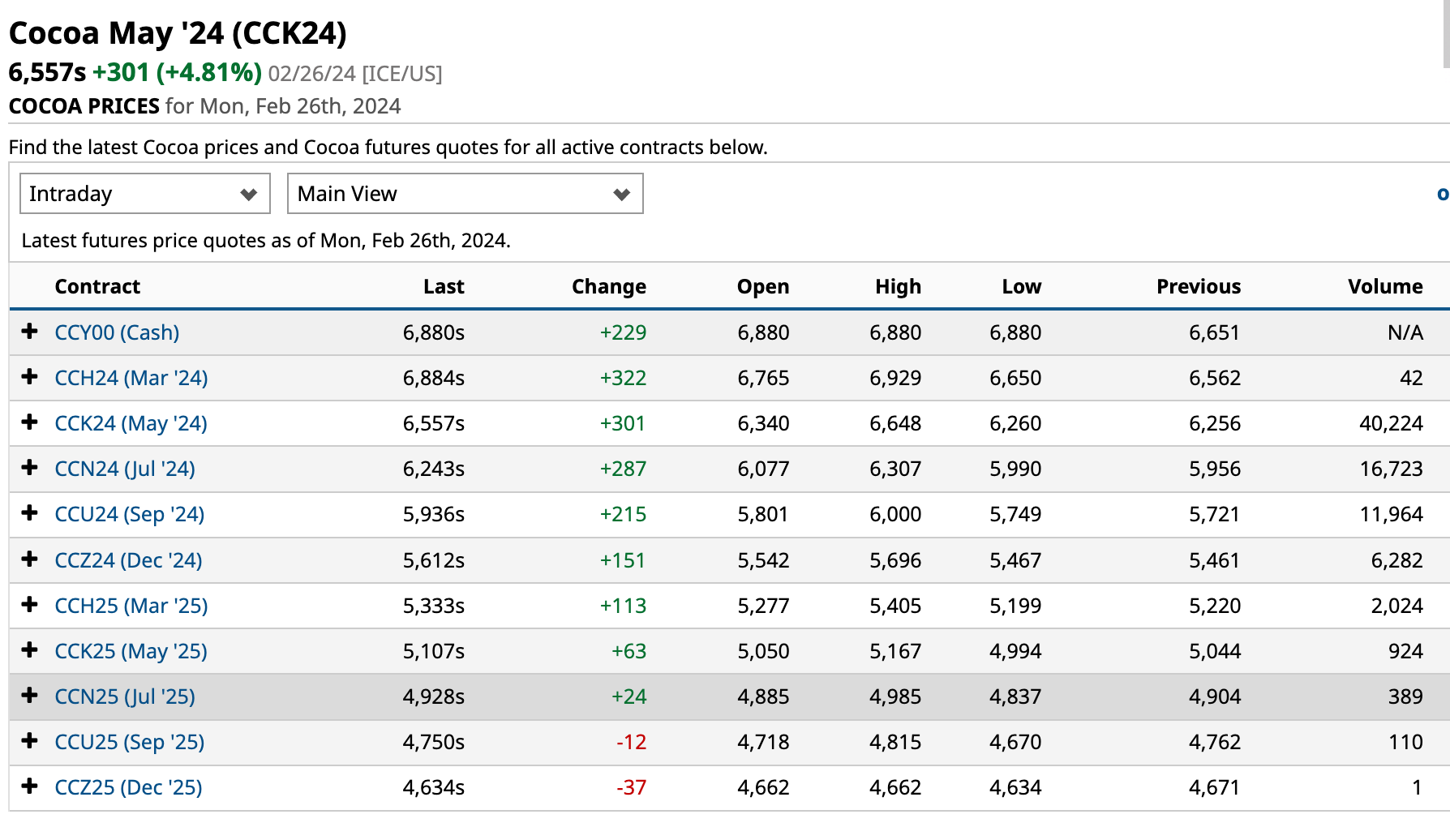

Commodity cocoa futures prices are at levels we haven’t seen in decades, with NY ICE futures trading at well over $3,900 per metric tonne (MT) the week of writing this post (Nov 6 2023). Prices will almost inevitably surpass $4,000 per MT very soon.

These futures prices are for bulk cocoa delivered to port in New York (there is a separate futures market based on London), at a range of near-term dates in the future (this is why they are called “futures” contracts). Commodity markets are often acknowledged as having “boom and bust” cycles, in which “boom” refers to times the price of the commodity experiences sustained increases, and “bust” meaning when the price drops significantly. There is no doubt that as of this post, in November 2023, we are in the midst of a boom in commodity cocoa prices!

Why? While some of the price increase is driven by intricacies of financial speculation on cocoa futures trading, there are significant physical factors driving these dynamics. Climate, disease, and productivity in Ghana and Cote d’Ivoire (which together produce over 60% of the world’s cocoa crop) are the primary focus. Here are some of the key drivers:

- 25% lower crop projected for this year in Cote d’Ivoire, in part due to widespread swollen shoot disease affecting up to 20% of production;

- Lower crop expected in Ghana due to black pod fungus resulting from heavier rains than normal earlier this year, and lack of fertilizer for farms to grow productivity;

- El Niño climate impacts, including prolonged hot and dry weather;

- A hangover ~145,000 MT deficit from the 2022/23 harvest.

In general, there is also strong and growing demand for cocoa. The International Cocoa Organization (ICCO) is projecting a +0.2% increase in cocoa grindings. The stocks-to-grinding ratio is projected to fall to a 7 year low of 34.5% by the end of the year, and overall another deficit of ~100,000 tons of cocoa is expected at the end of 2023.

Low supply + strong demand = higher prices. It’s (more or less) as simple as that, although the way these prices play out in global cocoa markets may not be quite so simple.

Are farmers earning more?

In general, yes, farmers are being paid higher prices this season, although we don’t know yet how total earnings will be impacted by lower production. The way these prices reach farmers (and the extent to which they do) varies by country, among other factors.

For example, in Ghana and Cote d’Ivoire, which together produce over 60% of the world’s cocoa crop, farmgate prices are set in advance of the season. That means farmers in those two countries already know the set price for all of their production this season. While both countries increased farmgate price before the current season started (Cote d’Ivoire by 11% and Ghana by 64%) as the market was already climbing, farmers will not capitalize on the higher market values during the season. This will likely cause an outflow of cocoa from these two countries to other countries where the farmgate price is dynamic and will be higher.

In Uganda, farmers are already receiving farmgate prices as high as $4,000/MT, a 65%+ increase over the previous crop. Prices are changing daily as buyers adjust to make sure they’ll be able to access the crop from farmers.

In Central America, where futures prices have the least important impact, we’re still seeing farmgate and export prices increase due to lower production driven by environmental factors, starting with the 2020 hurricanes Eta and Iota, from which many parts of the region have not yet fully recovered. The lower production is creating stronger local demand and competition to source for regional markets in Guatemala, El Salvador, and Mexico, leading to higher prices. In addition, inflated costs of living combined with lower productivity on their farms means farmers need to be paid more in order to continue focusing on their cacao farms instead of seeking alternative sources of income. The crop in much of Central America was down by 25%+ in 2023; 2024 is starting to show signs of improvement, but it is still too early to tell, and we are expecting higher farmgate and FOB prices from our partners this coming year.

In the Caribbean, the Dominican Republic’s 2023 harvest was cut unusually short due to climate factors, causing out of stocks and much lower production than expected. While the small harvest is now starting slowly, the coming season’s output is still unclear, and prices in the 2023/24 harvest are certain to be higher, essentially tracking trends in the futures market.

In South America, Ecuador has recently risen to become the third largest producer of cocoa globally after Ghana and Cote d’Ivoire, so futures prices are certainly driving up farmgate and export prices there, as well as in Peru. In Colombia, most of the country’s cocoa is processed into chocolate domestically, so futures market pricing has less influence, but currency volatility has driven up USD equivalent pricing and we are seeing significant jumps on FOB prices.

Across the board, in all countries where prices are climbing, quality control is becoming even more important, as farmers are incentivized to sell as much cocoa right now as they can. In-country buyers have to be particularly cautious around identifying lower quality (unripe pods, diseased or damaged pods) and manipulated (water or other material added in) cacao being sold.

What does it all mean?

This is an important and meaningful time for players across the cocoa value chain. Multinational cocoa buyers and traders are changing their tune on the market, refusing to pay current prices because of “too much risk” and saying they “can’t afford” to contract. This week, Bloomberg reported that major cocoa traders Cargill, Olam, and Barry Callebaut are refusing to contract at current prices. Hmmm… so the market isn’t always right?

Farmers and in-country exporters have borne the risks and hardships of lower prices for decades, and this author believes that a sustained increase in bulk cocoa pricing is long overdue. While the majority of those in the cocoa industry are anxiously waiting for the market to “cool off” and prices to drop, it seems to this author that oft-ignored externalities are finally taking a toll on the superficially perfect market, and prices may not be coming down anytime soon.

In the midst of a generally complicated geopolitical time in our world, with multiple high-stakes wars, dramatic climate impacts, and humanitarian crises, the dynamics of the commodity cocoa market represent a fascinating tangent of the complexities of modern civilization and the cumulative impact of recent centuries. Power is building and shifting along different parts of the value chain; without cocoa, there is no chocolate. Nobody really knows how this is all going to play out. For certain, we will see higher chocolate prices in 2024. But in the context of declining and volatile supply, perhaps we will see more willingness for decommoditization (divorcing prices from the futures market and engaging in more direct, stable price negotiation)? More “cost plus” strategies that truly take into consideration paying cacao producers at the very least a living income?

How will this impact me as a bean-to-bar chocolate maker?

Uncommon Cacao has already begun signing contracts for the 2024 harvest season, including in Ghana, where we are paying full market value + the Living Income Differential + country differential + $700/MT premiums for Fair Trade, Organic, and Quality. We have signed contracts in Uganda, where the FOB price of quality organic cacao is increasing by 20%. We have long argued that cocoa is undervalued, and are happy to be paying higher prices, ensuring quality remains excellent and that higher prices are making their way to farmers.

All of this to say that chocolate makers would be wise to plan ahead for rising costs of cacao this coming year. The price of ABOCFA will rise quite substantially, as well as other popular origins like Öko Caribe, Semuliki Forest, and Tumaco. We will be working diligently to ensure our efficiency as a business so we can offer you the best pricing, but please also keep in mind that if your volumes are declining, the price increase will be higher. We are committed to being a sustainable supplier and serving both cacao producers and chocolate makers over the long term. Please reach out to us soon to start planning your 2024 bean needs!

{kind=link}